Health Insurance Services

Health Insurance:

Health insurance is important for you and your family members. Making a smart health insurance choice can save you hundreds or even thousands in a year. We are experts in finding affordable health insurance plans that meet your needs. These affordable medıcal ınsurance plans have a wide range of deductibles and low cost premıums to fit your lifestyle needs and budget. Affordable health ınsurance quotes don’t have to be complicated. We make ıt simple. We also work directly with Market palace.

Why should I have individual health insurance?

- Prepare for the unexpected. You never know when you’ll need medical help.

- Staying healthy. Many preventive care services – like checkups - are covered at 100%.

- It’s the law. Under the Affordable Care Act, you may pay a penalty if you don’t have qualified health care coverage.

Health insurance is a good way to help you manage your health care costs. You pay health care companies premiums – a set amount of money each month - and you get benefits to pay for your eligible health care expenses. This can include regular doctor checkups or injuries to treatment for long-term illnesses.

When you’re self-employed, your time can feel stretched. A self-employed person, with no employees, you are considered an individual in the eyes of the government. This means you are now required to have health insurance or you could be subject to penalties come tax season. Whether you are a or starting your own business, the flexibility of today’s health care options makes it easier than ever to find a plan that works for you.

Health insurance for small business

If you are self-employed but have employees working for you, whether it is a small staff or team of up to 99, you are considered a small business. Choose from a great set of options, made to work for your small business.

**You can sign up at any time of year for Medicaid or CHIP (Children Health Insurance program), which are federal and state insurance programs for low-income families.

We serving State of Georgia with great Customer Service and always looking out for the best coverage, at the most reasonable price.

Medicare:

Medicare is a federal program, managed by the Centers for Medicare & Medicaid Services, that provides health insurance to eligible United States citizens and legal permanent residents of five or more continuous years.

You’re eligible for Medicare if you’re 65 or older or under 65 through disability. You may also qualify for Medicare at any age if you have end-stage renal disease requiring dialysis or a kidney transplant, or amyotrophic lateral sclerosis (also known as Lou Gehrig’s disease).

For Consultation please call or make appointment with our representative.

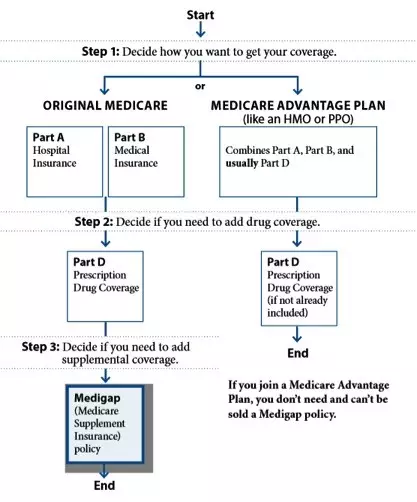

Which Medicare Option is best for you?

Part A– Hospital Insurance – this covers any services that you might receive in an inpatient center, such as a hospital, nursing facility, hospice or home care

MedicaPart A helps cover the services listed below when medically necessary and delivered by a Medicare-assigned health-care provider in a Medicare-approved facility

Blood transfusions

In most cases, the hospital gets blood from a blood bank at no charge, so if you receive blood as part of your inpatient stay you won’t have to pay for it or replace it. If the facility has to buy blood for you, usually you need to pay for the first three units you get in a calendar year or have it donated. Medicare Part A covers the cost of blood beyond the first three units you receive during a covered stay in a hospital, critical access hospital, or a skilled nursing facility.

Hospital stays

Medicare Part A generally covers hospital stays, including a semi-private room, meals, general nursing, and certain hospital services and supplies. Part A may cover inpatient care in:

- Critical access hospitals

- Inpatient rehabilitation facilities

- Acute care hospitals

- Qualifying clinical research studies

- Long-term care hospitals

- Psychiatric hospitals (up to a 190-day lifetime maximum)

Medicare Part A covers this care if all of the following are true:

- A doctor orders medically necessary inpatient care of at least two nights (counted as midnights).

- The facility accepts Medicare and admits you as an inpatient.

- You require care that can only be given in a hospital.

- The hospital’s Utilization Review Committee approves your stay.

Nursing home or skilled nursing facility

Medicare Part A covers limited care in a skilled nursing facility (SNF) if your situation meets a number of criteria:

- You’ve had a “qualifying inpatient hospital stay” of at least three days (72 hours). The time begins the first midnight after admission and does not include any hours on the discharge date.

- The SNF is Medicare-certified.

- Your doctor has determined you need skilled nursing care every day. This care must come from (or be directly supervised by) skilled nursing or therapy staff.

- You haven’t used all the days in your benefit period. (According to Medicare, this period begins the day you’re admitted to an SNF or a hospital as an inpatient, and ends when you haven’t had inpatient care or skilled nursing care for 60 consecutive days.)

- You require skilled nursing services either for a hospital-related medical condition, or a health condition that started when you were getting SNF care for a hospital-related medical condition.

Nursing home or skilled nursing facility stays must be related to your diagnosis during a hospital stay. For instance, suppose your hospital stay was for a stroke and your doctor determined that a nursing home or skilled nursing facility was medically necessary for your recovery. In that case, Medicare may cover a nursing home or skilled nursing facility stay for rehabilitation. A nursing home or skilled nursing facility stay includes a semi-private room, meals, and rehabilitative and skilled nursing services and care.

The coverage is limited to a maximum of 100 days in a benefit period. The first 20 days are paid in full, and the remaining 80 days will require a copayment. Medicare Part A will not cover long-term care, non-skilled, daily living, or custodial activities.

Swing beds

Certain hospitals and critical access hospitals have agreements with the Department of Health & Human Services that lets the hospital “swing” its beds into (and out of) SNF care as needed. The same cost-sharing and coverage rules apply as if these services were delivered in an SNF.

Home health services

Eligible home health services may include limited part-time care with services like intermittent skilled nursing care, physical or continued occupational therapy, home health aide service, speech-language pathology, and more. It may also include certain medically necessary in-home medical equipment (wheelchairs, hospital beds, walkers, oxygen), and other medical supplies.

Hospice care

Hospice care is for the terminally ill who are expected to have six months or less to live. Coverage includes pain-relief and symptom-control prescription drugs, medical and support services, grief counseling, and other services. Care is provided by a Medicare-approved hospice provider who will visit you at your home. Medicare also provides additional care for a hospice patient so that the usual caregiver can take a time of rest. Medicare may not cover all services that are provided to patients who receive hospice assistance.

Whatever health care insurance coverage you choose, make sure you have a clear understanding of all the options, coverage and premiums. Don’t be afraid to ask questions and seek a Medicare representative that can help you to fully understand and tell you what you will need to do to sign up.

Part B– Medical Insurance – Part B covers your doctor’s visits, outpatient care and some preventative Medicare Part B is medical insurance; coverage includes (but is not limited to):

- Medically necessary doctor services

- Screenings

- Ambulance transportation

- Outpatient hospital care, such as some physical or occupational therapy

- Mental health services

- Some home health care services

- Durable medical equipment

What is preventive care ?

Preventive care includes screenings and tests that help find health problems early so they can be treated. Some services, like flu shots and health education, may help prevent health problems.

Medicare Part B covers these preventive services:

- Alcohol misuse counseling

- Bone mass measurement (bone density)

- Breast cancer screening (mammogram)

- Cardiovascular disease (behavioral therapy)

- Cardiovascular screening

- Cervical and vaginal cancer screening

- Colorectal cancer screening

- Depression screening

- Diabetes screening

- Diabetes self-management training

- Flu shot

- Glaucoma test

- Hepatitis B shot

- Hepatitis C screening

- HIV screening

- Lung cancer screening

- Medical nutrition therapy services

- Obesity screening and counseling

- Pneumococcal shot

- Prostate cancer screening

- Sexually transmitted infections screening and counseling

- Tobacco use cessation counseling

- “Welcome to Medicare” preventive visit

- Yearly “Wellness” visit

Part C– Medicare Advantage – this provides some private insurance companies for you to choose from if you don’t want Medicare

A Medicare Part C (also called Medicare Advantage) plan is a private insurance policy that replaces Medicare Part A and Part B. In other words, if you enroll in a private Medicare Part C plan, you no longer receive coverage through Medicare Part A or Medicare Part B.

Services Covered

- Hospital stays

- Skilled nursing

- Home health care

- All the benefits of Part A, except hospice care

- Doctor’s visits

- Outpatient care

- Screenings and shots

- Lab tests

- All the benefits of Part B

- Prescription drug coverage is included in many Medicare Advantage plans, but not all.

- Eye care

- Hearing care

- Wellness services

- Nurse helpline

- Extras may be bundled with the plan.

Types of Medicare Advantage (Part C) plans

It's important to understand the differences between the types of Medicare Advantage plans to see which works best for you. There are several different types of Medicare Advantage plans:

- HMO (Health Maintenance Organization plan): Lets you see doctors and other health professionals who participate in its provider network. If your doctor is already in network, it could be a good option because you tend to pay less out-of-pocket with in-network doctors.

- PPO (Preferred Provider Organization plan): Covers both in- and out-of-network providers, giving you the freedom to choose any doctor that accepts Medicare assignment, which can work if you prefer that kind of flexibility.

- PFFS (Private Fee-for-Service plan): The plan determines how much it will pay providers and how much you must pay when you get care. The treating doctor has to accept the plan’s payment terms and agree to treat you. If the doctor doesn’t agree to those terms, then the PFFS plan will not cover services through that doctor.

- SNP (Special Needs Plans): Are especially for people who have certain special needs. The three different SNP plans cover Medicare beneficiaries living in institutions, those who are dual-eligible for Medicaid and Medicare, and those with chronic conditions such as diabetes, End Stage Renal Disease (ESRD), or HIV/AIDS. This type of plan always includes prescription drug coverage.

- HMO-POS (Health Maintenance Organization - Point of Service plan): Covers both in- and out-of-network health services, but at different rates. You pay less out-of-pocket when you go to in-network doctors, labs, hospitals, and other health care providers.

- MSA (Medical Savings Account plan): Includes both a high deductible and a bank account to help you pay that deductible. The amount deposited into the account varies from plan to plan. The money is tax-free as long as you use it on IRS-qualified medical expenses, which include the health plan's deductible.

Part D– Prescription drug coverage

Anyone on Medicare (with either Part A or Part B) is entitled to drug coverage (known as Part D) regardless of income. No physical exams are required. You cannot be denied for health reasons or because you already use a lot of prescription drugs.

You must enroll in one of the private insurance plans that Medicare has approved to provide it. Wherever you live, you can get drug coverage in one of two ways:

PDP Plans

A stand-alone Medicare Part D plan is referred to as a Prescription Drug Plan (PDP). Individuals are eligible to enroll in a Prescription Drug Plan if they are entitled to Medicare benefits under Medicare Part A and/or Medicare Part B.

This form of insurance helps pay for a variety of prescription drugs, including:

- Outpatient prescription drugs

- Vaccines

- Biologicals

- Some medical supplies not covered by Part A or Part B

MA-PD Plans

Those enrolled in a Medicare Advantage plan (Part C) can also choose prescription drug coverage. A Medicare Advantage Prescription Drug plan (MA-PD) is a Medicare Advantage (Part C) plan that includes prescription drug coverage.

MA-PD plans are offered by private companies that contract with Medicare to provide Part A, Part B and Part D benefits. Medicare Advantage Plans include Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), Private Fee-for-Service (PFFS) plans, or Medicare Medical Savings Account (MSA) plans.

What is a Medicare Supplement Plan?

Millions of Americans rely on original Medicare to help cover healthcare costs in retirement. Medicare is not costless of course: you will still be responsible for co-payments and deductibles. To help pay for these, you may want to buy a supplemental medical insurance policy known as Medigap. Medigap policies are offered by private insurance companies and are designed to cover costs not paid by Medicare. As you might guess by the name, Medigap can help you fill the gaps in your Medicare coverage.

Some Medigap policies also offer coverage for services that Original Medicare doesn't cover, like copayments, coinsurance, and deductibles. Some Medicare Supplemental insurance plans also cover certain hospital or medical services not covered by Medicare. Also like medical care when you travel outside the U.S. If you have Original Medicare and you buy a Medigap policy, Medicare will pay its share of the Medicare-approved amount for covered health care costs. Then your Medigap policy pays its share.

A Medigap policy is different from a Medicare Advantage Plan. Those plans are ways to get Medicare benefits, while a Medigap policy only supplements your Original Medicare benefits.

Each Medicare Supplement (Medigap) policy covers one individual. That means, you and your spouse would each need your own policy. We will help you understand what you and your family may need.

8 things to know about Medigap policies

- You must have Medicare Part A and Part B.

- If you have a Medicare Advantage Plan, you can apply for a Medigap policy, but make sure you can leave the Medicare Advantage Plan before your Medigap policy begins.

- You pay the private insurance company a monthly premium for your Medigap policy in addition to the monthly Part B premium that you pay to Medicare.

- A Medigap policy only covers one person. If you and your spouse both want Medigap coverage, you'll each have to buy separate policies.

- You can buy a Medigap policy from any insurance company that's licensed in your state to sell one.

- Any standardized Medigap policy is guaranteed renewable even if you have health problems. This means the insurance company can't cancel your Medigap policy as long as you pay the premium.

- Some Medigap policies sold in the past cover prescription drugs, but Medigap policies sold after January 1, 2006 aren't allowed to include prescription drug coverage. If you want prescription drug coverage, you can join a Medicare Prescription Drug Plan (Part D).

- It's illegal for anyone to sell you a Medigap policy if you have a Medicare Medical Savings Account (MSA) Plan.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}